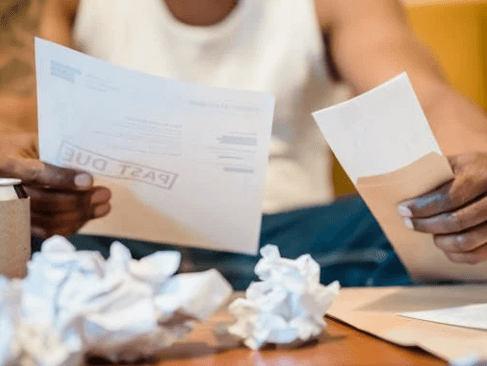

Did you know that missing just three to six mortgage payments could trigger foreclosure proceedings? Understanding the timeline for missed payments before foreclosure in Deerfield Beach, Florida, is crucial for homeowners facing financial difficulties. Statistics show that Florida remains one of the top states for foreclosure activity, making it essential to act quickly when you fall behind on mortgage payments. That’s where experts like Steve Daria and Joleigh, renowned real estate investors and cash house buyers, can offer solutions. They specialize in helping homeowners avoid foreclosure by providing quick and hassle-free options to sell their properties. By knowing the warning signs, deadlines, and alternatives, you can take control of your situation and safeguard your financial future. If you’re finding it difficult to keep up with your mortgage payments, take action now before the situation worsens. Book a free discussion with Steve Daria and Joleigh today to explore your options and learn how to successfully resolve challenges related to missed payments before foreclosure in Deerfield Beach, Florida.

What happens if I miss a mortgage payment in Deerfield Beach, Florida?

If you miss a mortgage payment in Deerfield Beach, Florida, your lender will typically notify you that the payment is overdue and charge a late fee.

Missing multiple payments may escalate the situation, potentially leading to consequences such as damaged credit scores or the initiation of foreclosure proceedings.

Generally, lenders wait until there are three or more missed payments before foreclosure in Deerfield Beach, Florida, but it’s crucial to act quickly to avoid further complications.

Contacting your lender promptly can help, as they may offer repayment plans or loan modifications to address the issue.

Ignoring the problem can further strain your financial situation and increase the risk of losing your home.

Additionally, consistently missed payments can have a lasting impact on your financial record, making it harder to secure loans in the future.

Proactively seeking guidance from professionals or housing counselors can help you explore alternatives, such as selling your property or refinancing.

Taking swift action is key to managing your situation and protecting your home and financial stability.

Get An Offer Today, Sell In A Matter Of Days

How long does the foreclosure process take in Deerfield Beach, Florida?

Are you facing foreclosure in Deerfield Beach, Florida? The timeline can differ depending on several important factors.

Typically, the foreclosure process begins after a series of missed payments, generally three to six months of non-payment.

Once initiated, lenders file a notice of default, informing you that legal action will begin if payments aren’t resolved.

The entire process can take anywhere from a few months to over a year, depending on whether the situation escalates to court proceedings or if delays, such as mandatory mediation, occur.

During this time, you may have opportunities to catch up on payments or explore alternatives, such as loan modifications or selling your home.

It’s worth noting that state laws and individual lender policies can impact timelines, so it’s important to act quickly.

For homeowners navigating missed payments before foreclosure in Deerfield Beach, Florida, understanding the steps and acting proactively is key to avoiding prolonged financial and legal challenges.

Seeking guidance from housing counselors or professional services can help you better manage the situation and find a resolution.

How many missed payments are there before foreclosure starts in Deerfield Beach, Florida?

- First Missed Payment: Missing your first mortgage payment usually prompts your lender to send a reminder notice and apply a late fee to your account. At this stage, reaching out to your lender to discuss repayment options or explain your situation is crucial to prevent the problem from growing.

- Second Missed Payment: After your second missed mortgage payment, your lender will likely increase their efforts to contact you, sending frequent reminders via mail or phone. During this period, the lender may begin alerting you to the potential for more serious consequences if the overdue payments are not addressed soon.

- Third Missed Payment: Three consecutive missed payments typically prompt your lender to consider your loan in default status, which is a formal step indicating more severe action may be taken. If you do not address the outstanding balance at this point, the lender can officially start the foreclosure process according to their policies.

- Notice of Default Issued: If you continue to miss payments, your lender will move forward by filing a Notice of Default—a document that signals the start of the official foreclosure process in Deerfield Beach, Florida. This document may incur additional legal fees and serves as a clear indication that you must act promptly to resolve your mortgage situation.

- Action from the Lender: Following the Notice of Default, your lender has the legal right to proceed with the foreclosure process if you do not take action to bring your account current or negotiate an alternative solution. The foreclosure proceedings may span several months, but responding quickly and seeking help early can make a significant difference in saving your home.

What options are available if I’m behind on payments?

If you’re behind on mortgage payments, there are several options to help you regain control of your situation.

The first step is to reach out to your lender quickly. They might offer options like a repayment plan or loan modification to help make your payments easier to manage.

If catching up on payments isn’t feasible, you could explore refinancing to lower your monthly costs or temporarily pausing payments through forbearance.

Some homeowners also consider selling their property to a cash buyer as a quick way to resolve their financial struggles and avoid foreclosure.

Alternatively, nonprofit housing counselors can guide you through budgeting and negotiating with your lender for better terms.

If you’re dealing with missed payments before foreclosure in Deerfield Beach, Florida, understanding timelines and acting early can help you protect your home.

Remember to remain proactive, as ignoring the situation can lead to more severe consequences, like foreclosure.

Each option depends on your specific financial circumstances, so weigh them carefully and seek expert advice if needed.

What are the risks of waiting too long before making a decision?

- Higher Financial Strain: The longer you wait, the more late fees and accrued interest you’ll have to pay. This can quickly add to your financial burden and make catching up even harder.

- Damage to Credit Score: Every missed payment negatively impacts your credit score. Delaying action can result in greater harm, making future borrowing more difficult.

- Loss of Options: Prolonged delays often mean fewer available solutions to your problem. You may miss critical opportunities, such as loan modifications or alternative payment arrangements.

- Legal Consequences: Delaying payment can result in legal action being taken by your lender. This might include formal foreclosure proceedings or the loss of your home altogether.

- Heightened Stress and Uncertainty: Putting off decisions increases emotional stress and uncertainty for you and your family. Acting sooner can provide clarity and potentially resolve the issue faster.

What documents will I need to complete a quick sale before foreclosure begins in Deerfield Beach, Florida?

To complete a quick sale before foreclosure begins in Deerfield Beach, Florida, you’ll need to gather a few essential documents.

First, ensure you have a copy of your mortgage statement to verify the outstanding balance and lender details.

Next, provide proof of ownership, such as the property deed, to confirm you are authorized to sell the house.

You’ll also need recent utility bills to show the property’s active status and good standing.

If applicable, include any homeowner association (HOA) documents to disclose fees or guidelines related to the property.

Tax records will also be required, as they help potential buyers assess potential liabilities or outstanding back taxes.

Additionally, having a government-issued ID on hand ensures seamless identity verification during the sale process.

For homeowners dealing with missed payments before foreclosure in Deerfield Beach, Florida, getting these documents ready quickly is vital for a stress-free transaction.

Steve Daria and Joleigh, seasoned real estate investors and cash house buyers, specialize in assisting homeowners with fast, efficient property sales.

Contact them today for a free discussion and take control of your financial situation before foreclosure progresses.

Takeaway

- Foreclosure can begin after just three missed payments. While some lenders may wait for up to 6 months, it’s crucial to act as soon as you miss your first payment to explore alternatives and avoid escalating penalties.

- Open communication with your lender is key. Many lenders offer options, such as repayment plans or loan modifications, that can help prevent foreclosure. Reach out early to show your willingness to resolve the issue.

- Florida foreclosure timelines vary but are often prolonged. The process can take months to over a year, which provides an opportunity to negotiate or sell your home. Acting quickly ensures you take advantage of these options.

- Foreclosure damages your credit and financial stability for years. A foreclosure can impact your ability to secure future loans or credit cards, making it even more challenging to regain financial stability. Taking early action can minimize this impact.

- Selling your home is an option to prevent foreclosure. Selling your property to a cash buyer is a fast and stress-free way to resolve missed payments and protect your credit. This option is especially helpful if other repayment plans don’t work for you.

**NOTICE: Please note that the content presented in this post is intended solely for informational and educational purposes. It should not be construed as legal or financial advice or relied upon as a replacement for consultation with a qualified attorney or CPA. For specific guidance on legal or financial matters, readers are encouraged to seek professional assistance from an attorney, CPA, or other appropriate professional regarding the subject matter.